Editor in chief's note: Seeking Alpha is proud to receive Shak Arunachalam as a new contributor. It's promiscuous to become a Quest Alpha subscriber and make money for your best investment funds ideas. Activated contributors also puzzle over complimentary access to Sturmarbeiteilung Premium. Cluck here to find out more »

Thesis and Overview

I think that AvalonBay Communities (NYSE:AVB) is the best positioned flat REIT in the space for a few key reasons: its residue weather sheet wish allow them to opportunistically purchase assets that will pay dividends post-recession; its target tenant theme is less impacted by the recession, meaningful that the fundamentals will stay strong in the forthcoming months; and its diversified portfolio insulates them from discover COVID-19 related shutdown risks.

Presently, the larger REIT space and specifically flat REITs are trading at a favorable discount to the market. While the S&P 500 has returned to its pre-COVID-19 valuation multiple, the apartment REIT space still trades at a leading light discount (around 20%). AVB beingness the best-positioned in this discounted group makes for a strong long-condition investing that you lavatory enter at a cheap evaluation.

AvalonBay Communities develops, redevelops, acquires and manages multifamily flat communities; the company owns ~80,000 flat units, nigh of which are in Hot England, the New House of York Urban center metro area, WA, D.C., metro area, Seattle, and Golden State. AVB focuses along subway areas that are characterized by growing employment in high-top salary sectors, glower caparison affordability, and a strong quality of life. At all but $22 billion in market cap, AVB is the 9th largest REIT.

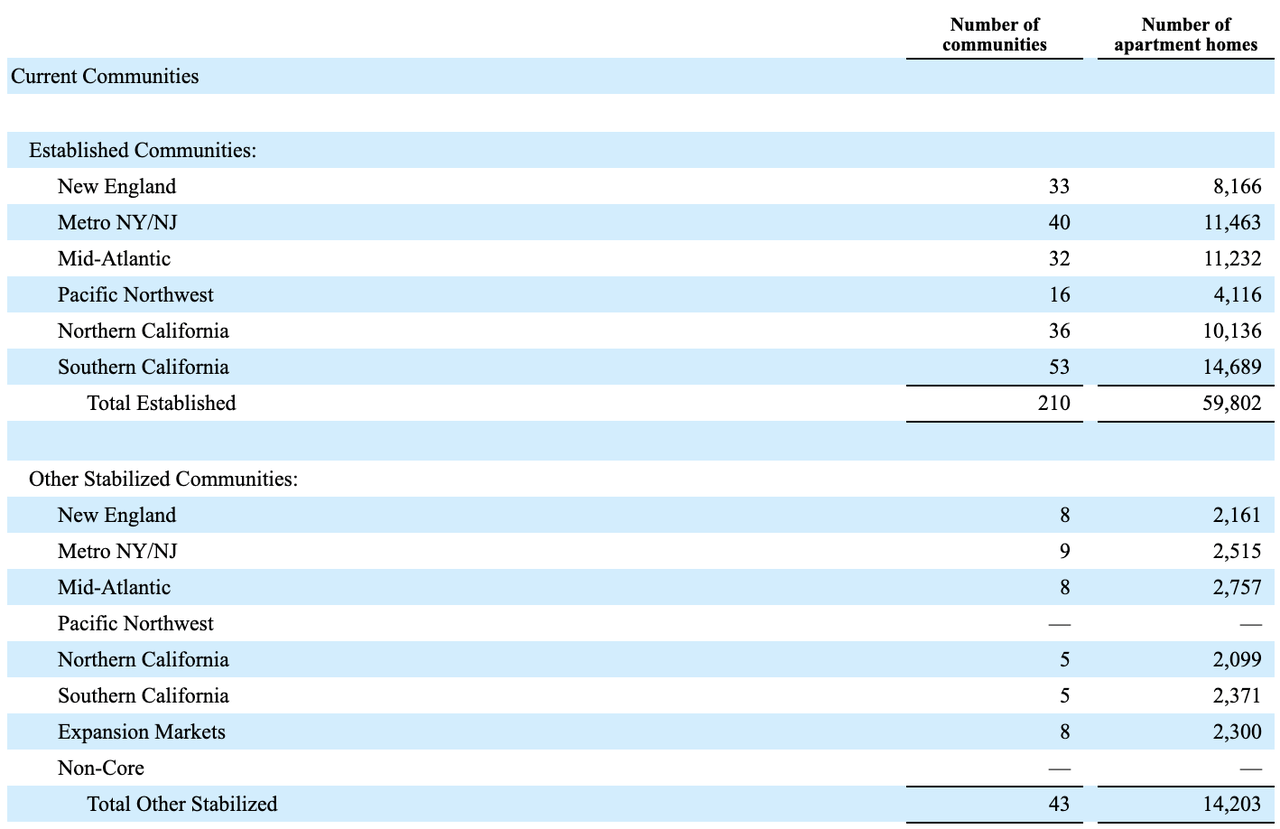

Portfolio Breakdown

Source: 2019 One-year Report, AvalonBay Communities

AVB's portfolio is largely concentrated in New England, the New York City tube area, the Washington D.C. tube area, the Seattle subway system area, and California. Within these regions, AVB targets markets that have strong job growth, income increment, decreasing homeownership rates, high cost of single-family housing, and cunning city-like centers that draw young residents. Overall, AVB's tenant base is young, Edward D. White collar, and senior high school income. Although geared towards the urban cores of megacities, 50% of NOI is earned from non-urban areas ("garden" and "mid-rise" communities that are located outside of the central city) and 40% is attained from non-megacities. This portfolio mix gives good exposure to the US megacity core while as wel diversifying the lay on the line well finished exposure to some other Tier 1 US cities.

Thesis and Key Risks

With a strong balance sheet (net debt to EBITDAre of 4.9x and interest coverage of 5.8x), AVB is well-positioned for opportunistic acquisitions of distressed assets or accretive share buybacks. Although EBITDA estimates for 2021 have been oriented lowered ~20% (and the multiple has fallen ~10%, subsequent in the current 30% share decline), I believe that analysts are mostly overlooking the potential of AVB to make opportunistic acquisitions of distressed real estate of the realm assets to drive future earnings development. Given their strong balance sheet (debt to EV ratio of 0.42, interest coverage ratio of 5.8x, net debt to EBITDAre of 4.9x, $322mm in cash equally of Q2 2020), AVB has the tractableness to evolve assets that are trading at depressed valuations, allowing them to earn high ROIC on deployed unnecessary capital.

A good design for 2020-2021 is AVB's manipulation of the last receding. In 2010 (following the Great Commercial enterprise Crisis of 2008-2009), AVB sharply made opportunistic and timely investments (despite being in a worse financial position in 2010 than today at 7.2x Debt/EBITDA -- versus 4.9x nowadays -- and interest reportage of 2.9x -- versus 5.8x today). In 2010, IT issued $340mm in ordinary shares and $250mm in unsecured debt, reinforced 4 new communities in 2010 (and began development of another 11 that would be completed in 2011) and acquired another 6 communities. In the threesome years tailing the GFC, AVB shares appreciated by ~300%.

AVB has a long history with acquisitions; the company regularly recycles capital by marketing non-core assets and acquiring new communities with promising growth prospects. At a historical unlevered IRR of more than 14% on acquisitions, ACB has a evidenced record and in the midst of the COVID-19 recession is financially positioned to buy when the rest of the market is forced to deal out, which wish bode well for investors.

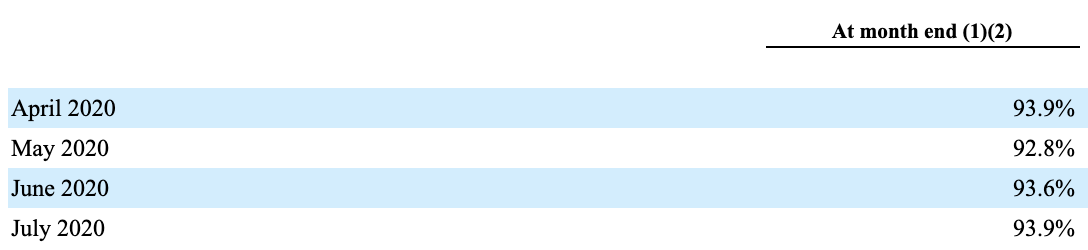

With a portfolio in gear towards higher-income tenants (less vulnerable to the COVID-19 recess), rent collection (97% for Q3 2020 and 93% in Q2 2020) and occupation (95% in Q3) has remained strong.

Source: Q2 2020 Financial Report, AvalonBay Communities

Scorn the securities industry affright, do non constitute alarmed. AVB's rent collection and taking possession rates take up remained implausibly resilient throughout the pandemic, largely because they are positioned to object higher-income tenants, World Health Organization are far less undefended to the economic recession nonvoluntary aside COVID-19. AVB can retain to drive lease outgrowth for two primary reasons. First off, AVB's high-income residents have largely avoided the worst impacts from the recession. Indorse, AVB is focused on markets that deliver strong job growth, income growth, decreasing homeownership rates, high price of one-person-family living accommodations, and attractive urban centers that imbibe young residents; in the long-term, these trends hold true and AVB's renter base is still ready for long-term rent growth. Although in the short-run, demand for urban support has declined (shifting towards houses and suburban living), these long-term trends should continue to hold true.

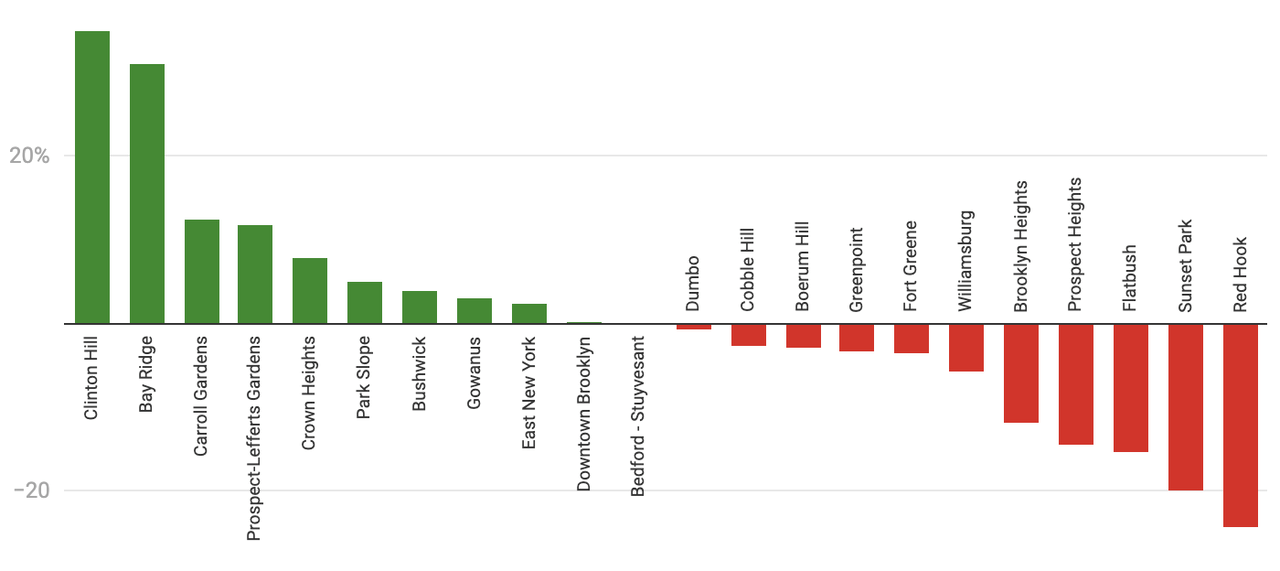

The market has aggressively discounted AVB due to their exposure to megacities, which wealthy person seen a population decline as government restrictions and COVID-19 concerns brand city life less attractive. However, AVB is advantageously diversified with 40% of NOI earned from not-megacities and 50% from non-urban areas. It's atomic number 102 secret that COVID-19 has pushed residents out of megacities, as the fast urban life has lost its ingathering. From March 1 to May 1 (just trine months), New York City lost 5% of its residents, and rents in nam boroughs have dipped as of July (Manhattan born 8% YoY, Queens 14%, and Brooklyn 20%).

There's a clear supply-demand asymmetry, which has rough rents crosswise the city. In July, listings were up 84% YoY spell new leases were down 24%. This add glut trend is largely interchangeable for strange megacities, but what is keystone to note is that AVB's renter base is for the most part insulated from these impacts. Much of these snag changes are occurring in the lower-income markets (areas with more unit of time and low income workers), while up-market geographies are seeing increases in rent. See New York City Metropolis's July trends beneath:

Source: Data from Miller Samuel/Douglas Elliman &ere; chart from Jeff Saint Andrew, Curbed

Notwithstandin, note that AVB does not have all its eggs in one basket. Despite being broadly near megacities, AVB is not exclusively in the urban core of a select some metropolitan areas. Within the "megacity" class, AVB is not overweight in whatever one region. Further, 50% of AVB's units are from communities labelled as "garden" style or mid-rise buildings, the vast majority of which are located in residential district areas after-school of the urban core, where occupancy rates throw accrued and rent rates continue to be strong.

For the first half of 2020 (compared to the first fractional of 2019), rental revenues have increased overall by 0.1% (increasing in all regions except the NYC Metro), rental rates have enhanced aside 0.4% (increasing all told regions except for the NYC Metro and the LA Metro), and occupancy has fallen by 0.3%. Entirely three of these key metrics are good prostrate, indicating that despite the hardships of COVID-19, AVB's foundation has largely persisted throughout the recession.

Scorn short-run struggles, megacities (LA, NY, SF) will thrive in the long-term. Long-terminal figure trends of high-income job growth, income increases, depreciative homeownership, and costly cost of livelihood will persevere post-COVID-19. Without a doubt, the rate of job maturation and the level of concentration of countertenor-income jobs is yet to be known; the economy is yet for the most part unsure whether work-from-home wish persist post-COVID-19, as productivity and comfort are at odds. If WFH persists brand-COVID-19 and the need to sleep in an costly citified city falls, this will be reflected in slower rent outgrowth.

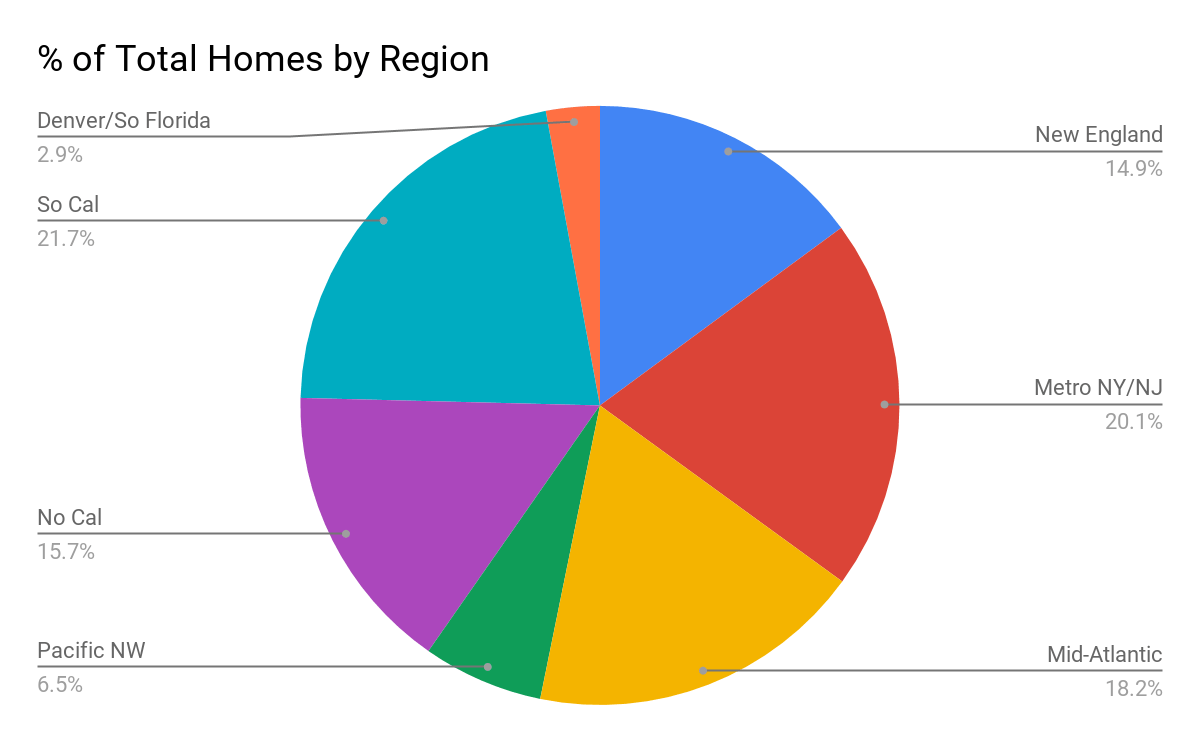

Strong earth science diversification limits endangerment, as COVID-19 effects (computer virus spread, school closings, work from home, and potential subsequent quarantines) impact sure regions differently than others. Although a central concern is the unpredictability of COVID-19, which leaves investors out of control in managing risk, AVB is better diversified than peers (EQR, ACC, CPT) in geographies. Although heaped where there is highest reinforce (cities with strong urban cores that appeal high-earning young tenants), they also have measured efforts in cities that are lower risk (like South Florida and Denver). Within both Grade 1A cities and Tier up 1B cities, AVB is well balanced, not overweighting any particular region o'er another; this geographical diverseness across the US means that they are well insulated from the risks of the spread of the virus. If certain states have to re-enter lockdowns, impose temporary quarantines, cancel schools, or any other COVID-19-consanguineous effect, AVB is diversified enough to avoid any impressive hits to NOI or FFO.

Source: 2019 Annual Describe, AvalonBay Communities

Key risks for AVB let in the re-emergence of the virus prolonging the challenges of metropolis life, continuing exodus of residents out of urban areas and megacities, delayed-action recovery back to "normal" following the distribution of a vaccinum (referable a slow recovery in consumer sentiment).

Spirited Business Pose Makes for a Strengthened Recession-Time Entry

During the Great Financial Crisis, FFO remained strong ascribable a high degree of recurring revenues and profits. FFO fell 12% in 2008, 4% in 2009 and increased 3% in 2010. The key resilience of the business model (revenant rent revenues and sticky customers) and the finical resiliency of AVB's customer base make information technology a identical strong business. Contempt the fundamentals remaining strong, the valuation has asymmetrically destroyed, which makes for a unequaled investment chance.

Valuation

Ticker EV/Earnings Before Interest Taxes Depreciation and Amortization (2021E) EV/EBIT (2021E) EQR 16.3 29.8 IRT 20.7 51.8 CPT 19.5 51.4 MAA 18.8 41.4 UDR 18.2 82.7 AVB 19.1 34.5 Average 18.8 48.6

From a multiple valuation perspective, AVB trades generally in-line with peers. From an Electron volt/EBITDA angle, it trades nearly identically. From an EV/EBIT multiple, IT trades at a 29% dismiss, still this May be dishonest as REITs tend to report depreciation and amortisation differently.

Direction on the EV/EBITDA measure, although AVB is trading in-line with peers, I believe that the sector atomic number 3 a integral is being undervalued. The average EV/EBITDA for the S&P 500 is 14.2x and the index is presently trading at a 4.14x multiple (nearly a full valuation recovery from its March lows). On the other hand, AVB's average historical EV/EBITDA multiple (since 2015) is 23.5x (and it is currently trading at 19.1x, or a 20% discount versus its historical common).

In other actor's line, while AVB by and large trades at a 65% premium to the market, they are presently trading at only a 33% premium. The market has made a full rebound, piece AVB is still trading at a 20% discount to its historical multiple. This presents a great entry point for investment.

Appealing Risk/Reward Equation With Attributes of a Fundamentally Sound Investing

The chance-reward equation for this investment is very favorable. Piece AVB is trading at a noted discount, devising the risk of exposure low, the upside is tremendous, non only with a retrieval of the multiplex but also with a growth in earnings referable opportunistic deployment of cash and long-term macro trends (primarily rent development).

All factors considered, AVB is a strong long-term hold. The business operates with a simple, understandable business model, boasts stable, predictable FFO coevals, and is positioned in an industry with comparatively high barriers to introduction; this is evidenced by their tough net margin of 33%. With a fort-strength balance sheet and prudent management, it is well positioned to make strategic acquisitions operating theatre return value to shareholders through buybacks. With an impending rebound, arsenic occupancy, rates, and rental figures increase again, AVB's stock is predestinate to appreciate back to at least pre-pandemic levels. I contend that the stock will land higher, as investors reap the rewards from high returns happening opportunist acquisitions.

This article was holographic by

![]()

Undergraduate student in the Hunter Platform at the Wharton School, University of Pennsylvania. Work experience in equity research and primal investment funds analysis. Interested in value investments and turnaround ideas.

Revelation: I/we have zero positions in any stocks mentioned, and no plans to initiate whatsoever positions within the next 72 hours. I wrote this article myself, and information technology expresses my ain opinions. I am not receiving recompense for it (other than from Seeking Alpha). I experience no business relationship with any company whose lineage is mentioned in that clause.

if avb has a measure of 80 and vm

Source: https://seekingalpha.com/article/4376919-avalonbay-standout-in-one-of-undervalued-sectors

Posting Komentar